{kind=link}

By Caribbean News Global ![]()

WASHINGTON, USA – Growth and quality job creation in Latin America and the Caribbean (LAC) remain subdued amid a challenging global environment. Inflation continues to decline, but monetary easing has proceeded more slowly than anticipated, non-energy commodity prices are softening, and persistent fiscal deficits continue to constrain needed investment. In addition, the rapid evolution of the global trade regime, together with heightened volatility in energy markets linked to the recent conflict in the Middle East, creates high levels of uncertainty around investment, inflation, and monetary policy undermining medium term growth prospects.

Frustration with a lack of progress on the longer-term growth and jobs agenda, combined with the emergence of new academic studies on the Asian Miracles has moved Industrial Policy back to the center of the policy debate in much of the developing world. While policy makers need to remain open to the emerging lessons, LAC’s historical experience—from import substitution industrialisation, through market-oriented reforms, to the recent return of industrial policy—shows that across sectors and policy regimes, weak productivity growth persisted, importantly because the region lacked the capability to identify and exploit new technologies, processes, products, and markets.

Hence, industrial policy needs to be thought of importantly as “learning policy,” with four agendas: building capabilities across the human capital spectrum; facilitating experimentation and risk-taking; exploiting openness productively; and, to redress the market failures attending each agenda, strengthening the state.

Revisiting industrial policy: Strategic options for today

Latin America and the Caribbean (LAC) enters 2026 with growth still constrained by long‑standing structural challenges. Regional GDP growth is projected to reach 2.1 percent in 2026—slightly below the 2.4 percent recorded in 2025—leaving LAC once again one of the slowest-growing regions in the world, with GDP per capita barely growing.

The lack of improvement comes with downward revisions in some country projections and reflects a familiar mix of demand: private consumption remains the main driver, while investment stays subdued amid elevated global and domestic uncertainty and still‑restrictive real (inflation-adjusted) financing conditions. Progress against inflation continues, albeit more slowly than expected. The changing global environment presents new risks and opportunities.

Though uncertainty surrounds the rules of the international trade order, tariffs on the region have risen less than expected, the potential remains for alignment with hemispheric production hubs, and the energy transition amplifies the region’s potential role in clean‑technology value chains, given LAC’s comparatively clean power mix and deep endowments of critical minerals. Realising these upside opportunities requires complementary domestic reforms that reduce policy uncertainty, close gaps in infrastructure and human capital, and strengthen institutions so that private capital can respond when global uncertainty recedes.

These upside prospects coexist with downside risks, notably from renewed conflict in the Middle East, where energy‑price volatility could delay disinflation and weigh on growth. Chapter 1 reviews the region’s recent macroeconomic and social evolution and the near‑term challenges it faces as inflation approaches its “last mile,” growth remains subdued, and fiscal space stays tight under high interest bills. Chapter 2 examines the reemergence of industrial policies that countries are experimenting with to instill more dynamism in their economies and create better jobs.

The state of the LAC region

- A dual‑track outlook in the Caribbean

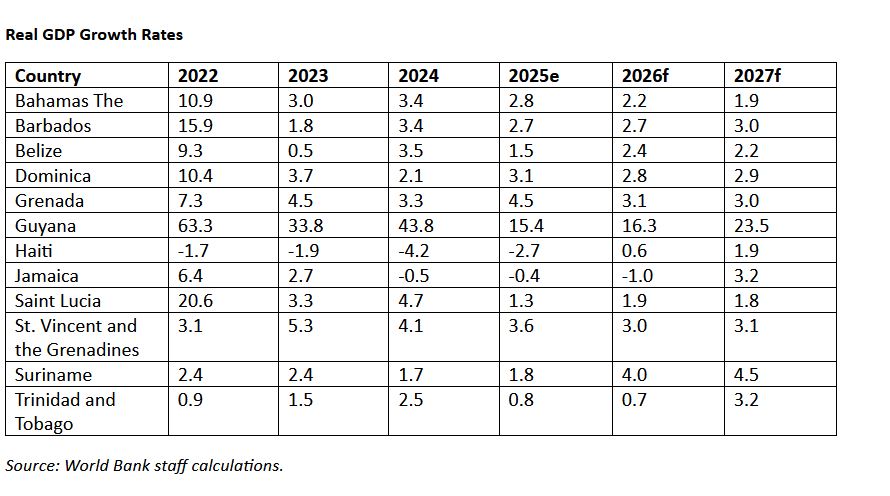

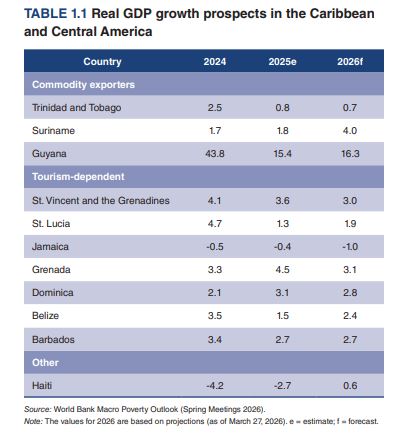

In the Caribbean, Guyana’s oil‑driven surge continues to lift the subregional average in 2026. Trinidad and Tobago—another hydrocarbon producer—benefits intermittently from gas‑related activity, but with a more mature production profile and without the scale of expansion seen in Guyana. Suriname, while not yet experiencing an oil‑led surge, is beginning to see growth supported by investment and expectations linked to recent offshore discoveries. By contrast, growth in the rest of the Caribbean has been moderating as tourism‑dependent economies face softer external demand, high import and energy costs, and climate‑related vulnerabilities. The result is an increasingly dual‑track outlook within the subregion. This widening contrast underscores the growing divergence between resource‑rich producers and the remainder of the Caribbean.

- Slow growth elsewhere

Without a broader reduction in uncertainty and real financing costs, and against a near‑term global backdrop shaped by developments in the Middle East, the region’s acceleration is likely to remain measured rather than broad‑based. Beyond these pockets of strength, most of the region has continued to grow only slowly in 2026. The combination of easier financing conditions in early 2026 and favourable commodity prices remains insufficient to overcome the drag from persistent trade tensions, policy uncertainty, limited fiscal buffers, and weak private demand.

Within this environment, Brazil is expected to cool further relative to 2025, as tight financial conditions—policy rates remained restrictive through early 2026—and a soft external environment weigh on credit, investment, and trade. A more discernible improvement will be likely only if monetary conditions normalise and global pressures ease.

Mexico’s low growth from 2024 is also likely to persist into 2026, as the fading impact from large public infrastructure projects coincides with ongoing uncertainty about trade policy. While the monetary policy easing cycle should lend some support to domestic demand, it will probably only partially offset external headwinds, particularly with reviews related to the United States-Mexico-Canada Agreement (USMCA) affecting the planning horizons of firms.

- A changing risk–opportunity profile amid heightened global uncertainty

Despite persistent structural headwinds and currently subdued growth expectations, LAC enters 2026 with a distinct and evolving risk–opportunity profile. The region remains far from active theaters of interstate conflict, providing a comparatively stable external security backdrop—even as violence linked to organised crime continues to pose challenges in several countries.

Caribbean and Central America

Some Caribbean and Central American economies outperformed Latin American countries in 2024, although performance continued to vary markedly between tourism‑dependent countries and commodity exporters (refer to table 1.1). Tourism‑based economies have broadly recovered the levels of GDP that prevailed before the COVID-19 pandemic, supported by the strong rebound in tourist arrivals, even as growth in the services sector is expected to moderate. Among commodity exporters, Trinidad and Tobago and Suriname experienced sharp output contractions during the pandemic following declines in international commodity prices, but activity has rebounded alongside the recovery in prices. Guyana stands out within the region, having recorded exceptionally rapid and sustained GDP growth since 2020, driven by the scaling‑up of offshore oil production.

This expansion has been accompanied by rising fiscal revenues, improved external balances, and a declining public debt‑to‑GDP ratio, although the pace of growth also underscores the importance of strengthening public investment management, building institutional capacity, and ensuring that oil wealth translates into broad‑based and inclusive development. Beyond near‑term macroeconomic dynamics, longer‑term challenges remain across the region, particularly related to productivity and labor mobility. These longer‑term constraints are particularly acute in Haiti, where repeated shocks have severely eroded household welfare and access to basic services.

- Box 1.2 takes a closer look at recent evidence from high‑frequency phone surveys, documenting how food insecurity, declining incomes, and service gaps have compounded development challenges in Haiti, read more page 21.

Public debt dynamics remain heterogeneous across the Caribbean and Central America. Several countries have reduced debt‑to‑GDP ratios through a combination of economic growth and fiscal consolidation. Relative to benchmarks before and during the pandemic, Belize, Costa Rica, Jamaica, Saint Lucia, Barbados, and Suriname show substantial progress in lowering debt burdens (refer to figure 1.19). Jamaica strengthened its fiscal governance framework in 2025 by making the Independent Fiscal Commission (IFC) fully operational, building on the foundations established by the Economic Programme Oversight Committee (EPOC).

The IFC’s early independent assessments of budget credibility and fiscal performance have reinforced steps toward transparency and policy credibility, supporting Jamaica’s transition to a durable, rules‑based fiscal framework. In Costa Rica, declining debt ratios reflect a more gradual, rules‑based consolidation anchored in the fiscal rule and expenditure controls, supported by sustained primary surpluses and improved market confidence.

This framework has helped stabilise public finances following the pandemic‑related increase in debt and strengthen fiscal credibility. Barbados and Belize reduced debt through decisive policy choices rather than gradual adjustment alone. Barbados combined fiscal reform with a comprehensive debt restructuring that lowered interest costs, while Belize cut external debt through a debt‑for‑nature swap tied to marine conservation. In both cases, visible actions helped lock in credibility and support the recovery.

At the same time, some highly indebted Caribbean economies continue to face challenges in achieving durable debt sustainability, while oil‑producing countries such as Guyana confront the parallel task of managing revenue volatility and avoiding procyclicality as public finances expand rapidly.

Inflation rose sharply across the Caribbean in 2022, driven by higher global food and fuel prices, although countries with exchange rate pegs were better able to cushion these shocks than those operating under inflation‑targeting regimes. Since 2023, the normalisation of international prices has contributed to a broad easing of inflationary pressures across the region (refer to figure 1.20).

Against this backdrop, recent developments related to the conflict in the Middle East introduce additional uncertainty for Caribbean and Central American economies through several distinct channels. Exposure differs across countries depending on their position in energy and food markets. At the same time, for economies whose growth models rely heavily on services—particularly tourism—shifts in global demand, air‑travel costs, and a more cautious short‑term global environment represent an additional source of vulnerability. Where these channels intersect, external shocks may compound, underscoring the sensitivity of growth prospects to global developments and reinforcing the importance of resilience‑building policies, diversification, and adequate buffers.

- Labor markets, informality, poverty, and inequality Economic slowdown constricts the decline in poverty, read more page 23.

How trade agreement frameworks shape the trade-off between autonomy and integration

At a broad level, three stylised frameworks illustrate the trade-off between autonomy and integration. Customs unions—such as the EU, MERCOSUR, and (in intent) the Caribbean Single Market and Economy (CSME)—adopt a common external tariff (CET) and a shared external trade policy. This model can deliver deep internal integration but typically limits members’ ability to pursue independent tariff‑liberalising agreements with third parties.

In return, it enables freer and more efficient intra‑bloc trade—by eliminating rules of origin—supports deeper production integration and bloc value‑chain formation, and strengthens collective bargaining power vis‑à‑vis external partners. Mega Free Trade Agreements (FTAs)—such as the Pacific Alliance and the CAFTA-DR (Dominican Republic–Central America–United States Free Trade Agreement) — occupy an intermediate position because they liberalise trade within the bloc while preserving members’ formal authority over external tariffs and third-party negotiations.

In practice, however, coordination requirements, complex rules of origin, and bloc-embedded supply chains can still constrain autonomy. Stand-alone FTAs, exemplified by Chile’s sequential approach, preserve the greatest formal autonomy and flexibility. Retaining control over tariffs and negotiating priorities facilitates diversified integration across partners, helping explain broader diversification rather than bloc-centric concentration.

Key options to deepen trade integration in LAC

Different options exist for different types of countries and markets. For the many LAC economies that are not bound by a customs union, the policy implication is straightforward: use full autonomy over external tariffs and negotiations to expand deep agreements with large, complementary markets. Chile is the clearest demonstration of this “autonomy leads to diversification” model: it has negotiated a very large set of trade agreements spanning a wide set of partner economies and a large share of world GDP, illustrating how a small economy can “buy” market size through sequential, high-quality agreements.

A similar outward strategy is being deployed in Peru, Colombia, and Costa Rica, which have built broad networks covering major global partners to secure predictable access and rules. The actionable message for this group is to prioritise agreements that materially expand exposure to large markets where complementarity is high, and pair them with trade facilitation and services/investment disciplines that improve utilisation.

For LAC economies bound by customs union rules—most prominently MERCOSUR—the feasible path to deeper integration is necessarily more institutional. One route is the bloc‑level “big bet”: negotiate and implement a deep agreement at the customs union level with a major partner. The EU‑MERCOSUR process exemplifies this approach: negotiations reached political agreement on the trade pillar in late 2024 and have moved into a ratification pathway.

Such an agreement would be consequential precisely because it would combine a step‑increase in GDP coverage—given the EU’s weight in global output—with preferential access to some of the markets with the highest purchasing power in the world (refer to the shaded areas in figure 1.25, panels D and E). A second route—often more tractable in the short term—is to pursue targeted, functionally deep cooperation that reduces non‑tariff barriers and improves certainty with key partners. Recent initiatives between the United States and Argentina illustrate this template, focusing on market access, standards, and barrier reduction through bilateral

frameworks. This channel is particularly relevant in settings where tariffs are already constrained or adjustment through tariffs is limited, and where non‑tariff and regulatory barriers tend to be the binding margins for trade. These options matter because MERCOSUR’s internal trade intensity is relatively low—about 10 percent of total trade — making external deals and mechanisms to reduce barriers particularly valuable.

Finally, there is an additional tailwind for renewed optimism: LAC’s strategic value in critical minerals is rising. Current estimates suggest that the LAC region concentrates around 50 percent of global lithium resources. This concentration of resources strengthens the economic logic for deepening market access and rules-based partnerships—not only on what LAC exports today but also on the region’s growing role in inputs critical to the global energy transition. All these routes promise additional trade opportunities, providing the region with a pathway toward more robust and diversified integration into the global economy.

- Full Report – Latin America & the Caribbean Economic Update | APRIL 2026