{kind=link}

- At the 2023 Arkansas State University Agribusiness Conference, Jonesboro, Arkansas – the opportunity to talk about where the economy is heading, what the Federal Reserve is doing to get inflation back down to our 2 percent goal, and how all that is likely to affect American agriculture.

By Governor Christopher J. Waller

The big picture is that the US economy is adjusting well so far to the higher interest rates that are necessary to rein in inflation. But inflation remains quite elevated, and so more needs to be done. Although economic activity slowed in 2022, I expect the Fed will need to keep a tight stance of monetary policy for some time to slow activity further in 2023. That is what I believe is needed to bring demand and supply into better alignment and lower inflation toward the Federal Open Market Committee’s (FOMC) 2 percent target. Some believe that inflation will come down quite quickly this year. That would be a welcome outcome. But I’m not seeing signals of this quick decline in the economic data, and I am prepared for a longer fight to get inflation down to our target.

So, what is my take on the recent data? It looks like the economy grew at a solid pace in the final quarter of the year, the labor market remained tight, and inflation continued to retreat. After adjusting for inflation, personal consumption grew at around a 2 percent rate, though it contracted in the last two months of the year amid some pretty significant headwinds.

One of those headwinds was high inflation, including for food and agricultural products. After accounting for inflation, spending on food consumed at home fell in 2022 after rising strongly in 2020 and 2021, the effect of both large price increases over the past year and the normalization of spending on groceries, which surged when people stayed home during the pandemic and reversed when they returned to restaurants.

Looking forward, I expect personal consumption will grow modestly and price increases will moderate, and I think such outcomes would bode well for the agricultural sector this year. It looks as though economic activity may be moderating further in the first quarter of 2023, but I expect the U.S. economy to continue growing at a modest pace this year, supported by a strong labor market and by encouraging progress in lowering inflation.

Though we have made progress reducing inflation, I want to be clear today that the job is not done. Inflation is still too high relative to the price stability goal of the dual mandate assigned to the Federal Reserve by Congress. The Fed has defined that goal as 2 percent annual inflation, as measured by the change in the price index for personal consumption expenditures, but another yardstick you could use is when high prices for groceries and other things are no longer front page news, and when farmers can worry less about rising costs for fertilizer and other inputs.

That is where we intend to get to, and thus the FOMC last week increased the target range for the federal funds rate by another 25 basis points, to 4-1/2 to 4-3/4 percent. Our intention is to tighten financial conditions, including raising the cost of credit, to dampen demand and spending to further reduce inflation. Of course, we know that higher interest rates pose challenges for farmers and ranchers who must borrow to smooth out the costs and returns from agriculture over the year. But excessive inflation is a larger challenge because it has the potential to become a lasting problem weighing on economic growth, undermining living standards, and hurting consumers, who farmers depend on.

That is why I am determined to get the job done, get high inflation off the front pages, and back to being something that households and businesses don’t think too much about when making decisions.

Continued upward pressure on inflation comes, in part, from a very tight labor market. The Job Openings and Labor Turnover Survey for December continued to show that the demand for workers remains robust, with job openings increasing by over 500,000 at the end of last year. Based on last Friday’s initial estimate, we learned that the US economy created a whopping 517,000 jobs in January, 330,000 more than the solid growth that was expected by economic forecasters. Furthermore, the unemployment rate ticked down to 3.4 percent, the lowest level since 1951.

Such employment gains mean labor income will also be robust and buoy consumer spending, which could maintain upward pressure on inflation in the months ahead. For employers, the very strong labor market makes it hard to find and retain workers. One effect of this tightness is seen in wages and other compensation, which ultimately show up in the prices that consumers pay for goods and services. For example, last year the Employment Cost Index (ECI), which tracks movements in labor costs, including both wages and benefits, increased over 5 percent, the highest rate since 1984. We want to see wages grow but at a pace that is consistent with our goal of stable prices.

We have seen some moderation in compensation growth in recent months but not enough. The ECI for hourly compensation for private industry workers increased at an annual rate of 4 percent over the three months ending in December, a step down from the 4.3 percent gain recorded over the three months ending in September and the 6.3 percent increase in June but still a strong increase. More recently, the 12-month change in a narrower measure of labor costs, average hourly earnings, was about 4-1/2 percent in January, continuing its slow deceleration from 5-1/2 percent last summer. The data are moving in the right direction, but I will watch for further slowing because we don’t want excessive wage increases to be a potential source of higher inflation in the future.

So now let’s talk about inflation. I will start with overall inflation and then focus on the different components, including food. I will talk about what those components can tell us about the direction of overall inflation and how I look at the different parts of inflation in my approach to monetary policy.

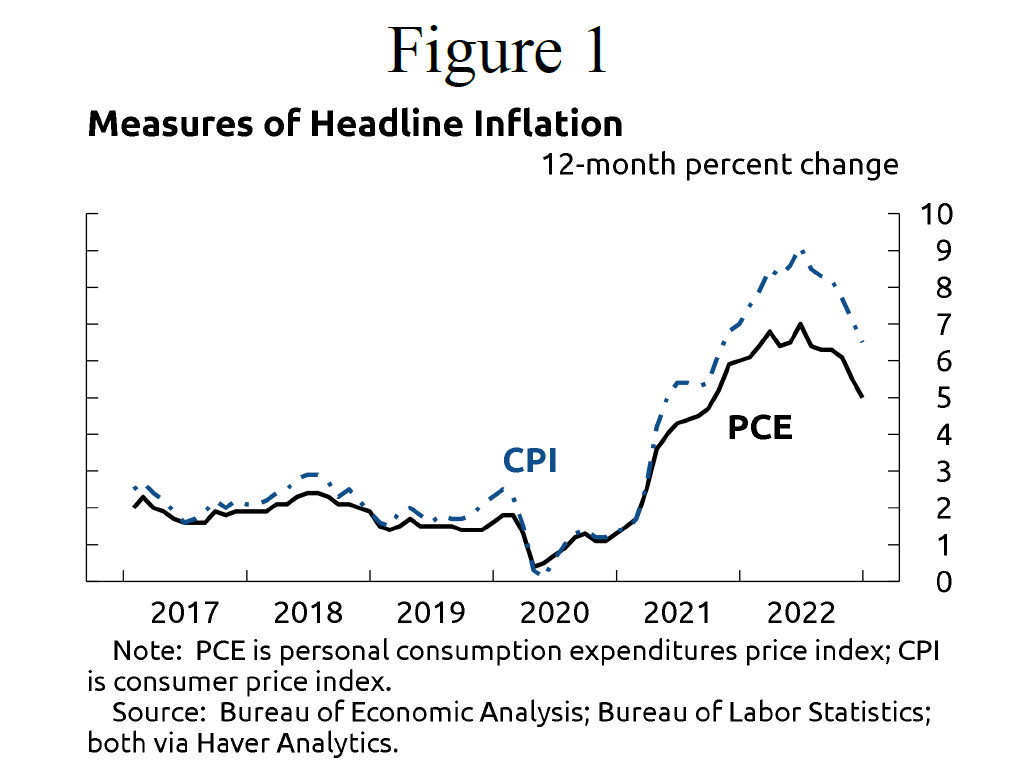

Figure 1 depicts inflation measured by two common indexes. No matter how one measures it, inflation has been running too hot for too long. “Overall” or “headline” inflation indexes are measured as the rate of increase in the average price level of a broad group of goods and services, called a market basket. Government statistics on the inflation rate will be a function of the specific goods and services included in the market basket. Including a different set of goods and services in the market basket will result in a different overall inflation rate.

{kind=link}

Probably the most often-discussed inflation measure in the United States is one based on the consumer price index (CPI). The CPI is widely used as a cost-of-living index to adjust Social Security and other payments. The CPI puts considerable weight on the prices of food, energy, and shelter. These three items account for about 50 percent of the expenditures in the CPI basket.

A second measure that is frequently watched is the one I mentioned earlier, the personal consumption expenditures (PCE) price index, which places less weight on food, energy and shelter—they make up about 30 percent of the expenditures in the PCE basket. The FOMC chose the PCE index over the CPI for its inflation target in part because it includes a broader set of goods and services in its market basket and is widely believed to better capture changes in the mix of goods and services purchased by consumers.

Monetary policy works with a lag, and after the Federal Reserve started raising interest rates last March, inflation peaked in the middle of 2022 and has been falling gradually since then. Twelve-month PCE inflation hit a high of 7 percent in June but ended the year at 5 percent. By comparison, over the final three months of 2022, headline inflation was much lower, running at an annualized rate of just 2.1 percent. The difference between the three-month and 12-months changes is a signal of ongoing moderation. As has been the case since the summer, falling energy prices are a big reason for lower inflation in the last few months, though food price inflation also moderated in the final few months of 2022.

These improvements are welcome news, but we need to keep them in perspective. As we can see in the figure, though PCE inflation is down from its peak, it is still quite elevated. And while the recent trend is encouraging, the improvements over the past year have been coming in ebbs and flows and it likely will continue this way. I need to be confident that inflation is declining in a sustained manner towards our 2 percent target, so I will need to see continued moderation in inflation before my outlook changes.

So where do I think inflation is heading? You will often hear economists talk about core inflation, which strips out energy and food prices, which tend to be volatile. The core measure is considered a better guide to the direction of future inflation. You might wonder why it is that the Fed doesn’t just target core inflation in measuring progress toward our price stability goal. There are some good reasons for keeping the focus on overall inflation, and in front of an audience of people who pay a lot of attention to food price inflation, I thought I would take a couple minutes to explain why I consider food and all of the components of inflation to be so important in my approach to setting monetary policy.

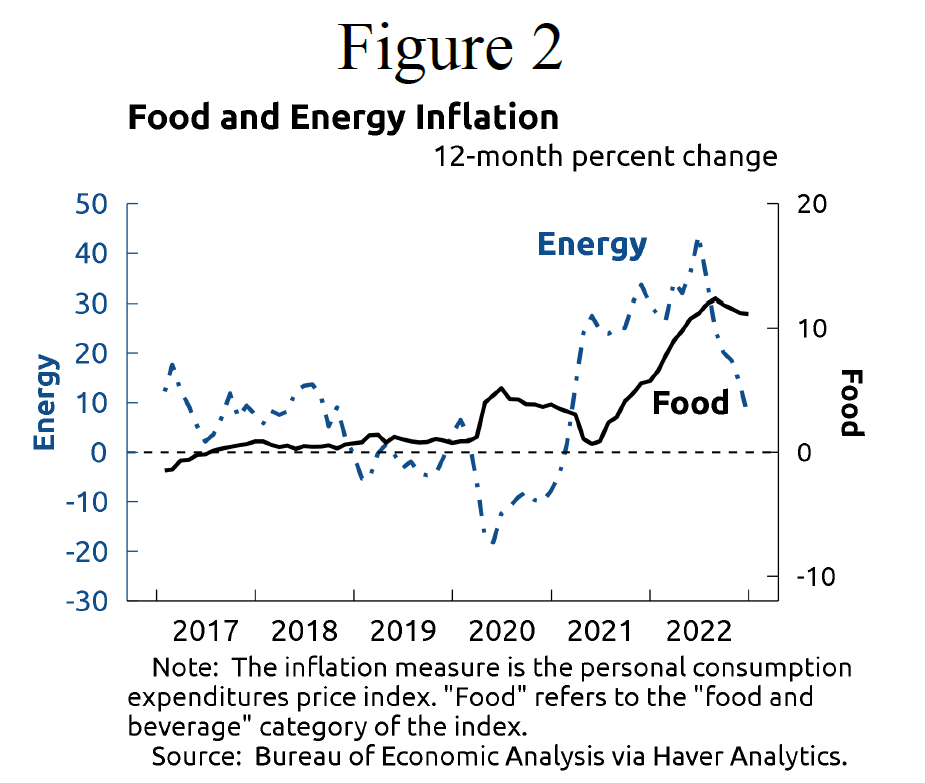

The argument for stripping out food and energy prices is that they tend to be quite volatile, with big ups and downs tending to equal out over time, and thus do not provide a clear signal of how inflation in these categories will evolve. One can see the recent volatility in figure 2 that reports 12-month rates of inflation for food and energy. Energy prices were decreasing for most of 2020 (they fell 10 percent during that period) but then switched to very large increases in 2021 and the first half of 2022. In mid-2022 we saw energy prices up about 40 percent from the year before.

{kind=link}

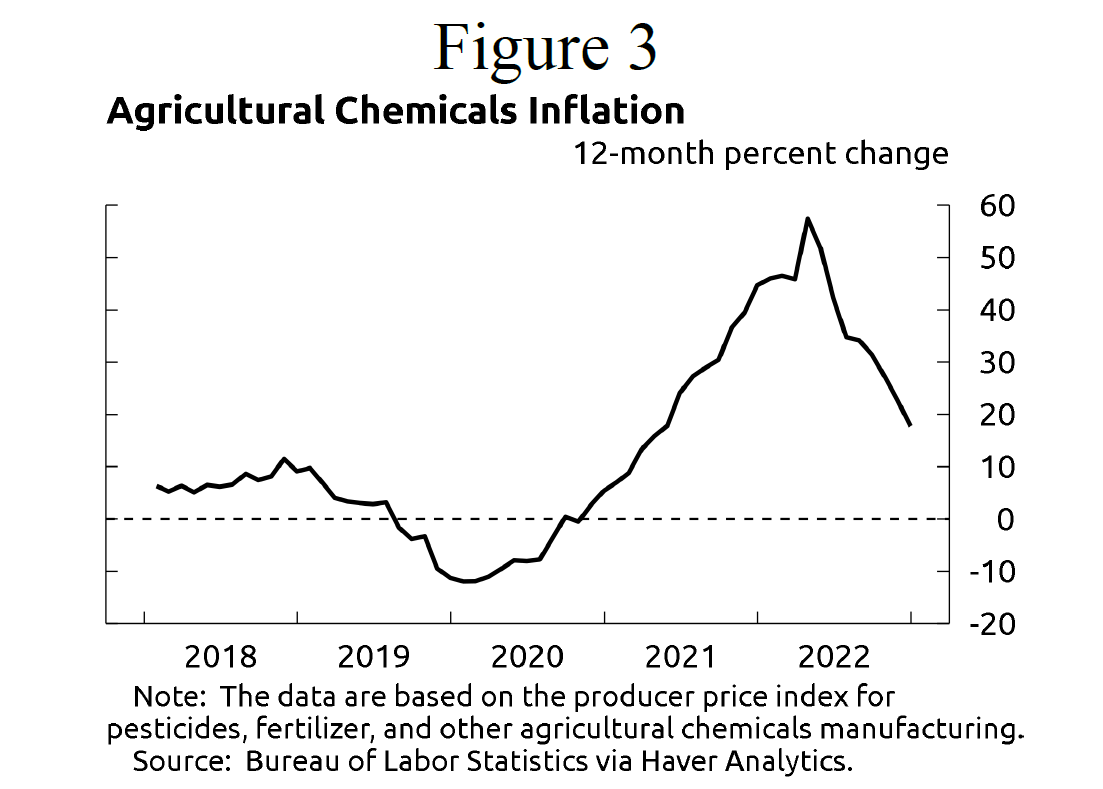

By December, that retraced to less than a 7 percent increase over 2021. And I’m sure I don’t have to tell anyone that food inflation has been quite high relative to its pre-pandemic average. Of course, food prices haven’t increased as much as energy prices, but food inflation has risen notably in 2021 and 2022 and has been running above 10 percent recently, which is unusually high. I know that farmers have been dealing with sharply rising input costs, and that is a significant factor driving up wholesale and retail prices for many food products. As shown in figure 3, inflation for agricultural chemicals, such as fertilizer, skyrocketed in 2021 and continued up in early 2022 and, though this inflation has moderated in recent months, the price level of agricultural chemicals remains very high.

{kind=link}

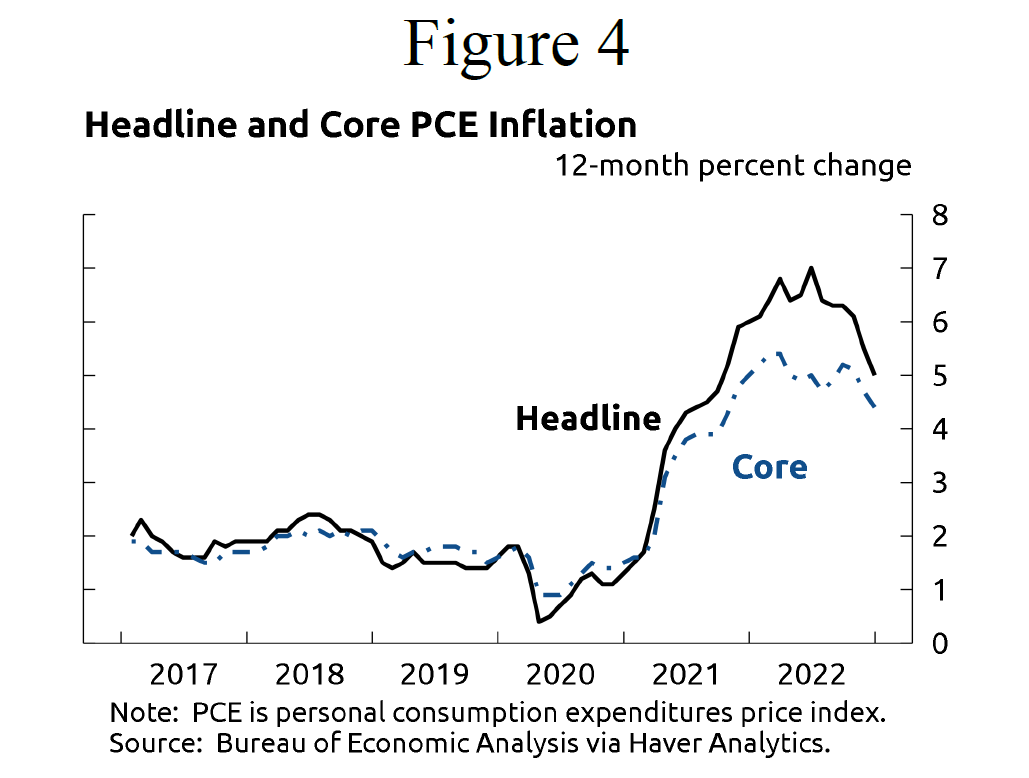

Core inflation, as shown in Figure 4, didn’t rise as much as headline inflation in this recent period of high food and energy price increases, and lately it hasn’t moderated as much. Core inflation stood at 4.4 percent in December, over double the Fed’s 2 percent target for headline inflation. Core inflation includes a measure of housing services, which is what households pay for rent or the equivalent for those who own their homes. Housing services inflation has been stubbornly high for all of 2022 and is a big factor driving up core inflation. There is good reason to believe rents will moderate significantly over this year and so some people have suggested that the focus should be on a “super core” measure of inflation that excludes food, energy, and housing. That would make inflation look not nearly as bad over the last year or two and also likely not show much improvement in the coming months.

{kind=link}

But there are a few reasons why I don’t let these stripped-down measures of inflation shape my views of the inflation environment. First, yes, historically food and energy prices have been volatile, and it has not been unusual to see price increases followed by price declines over fairly short periods of time, but that isn’t the recent history. In the last two years, prices for these goods and services have been moving largely in one direction-up-and even the decline in energy prices we saw in the second half of 2022 hasn’t offset the huge increases earlier.

The second reason that I wouldn’t exclude food, energy, and housing prices, or want to move toward a narrower inflation target, is that, by any measure of headline inflation, they constitute a large share of expenses paid by people. Excluding this large share of consumer spending doesn’t give you an accurate picture of what consumers are facing in their everyday lives, and that is a perspective that policymakers should never forget.

The third reason to include, rather than exclude, these prices in considering inflation is that they make up an even larger share of expenses for lower-income people, who have less savings and other means to deal with the ups and downs of their finances and the economy. Recent research indicates that the share of overall spending that lower-income households dedicate to food, energy and housing is about 1.2 times (or 20 percent more) than the share spent by higher-income households. Because of this disparity, when inflation peaked last summer, lower-income households effectively faced inflation that was a percentage point higher than was paid by higher-income households.

Lastly, and this is really the bottom line, the Fed has stated that its target for inflation is headline PCE prices. So, to meet the Fed’s price stability objective, policymakers are accounting for all the categories of goods and services that affect households.

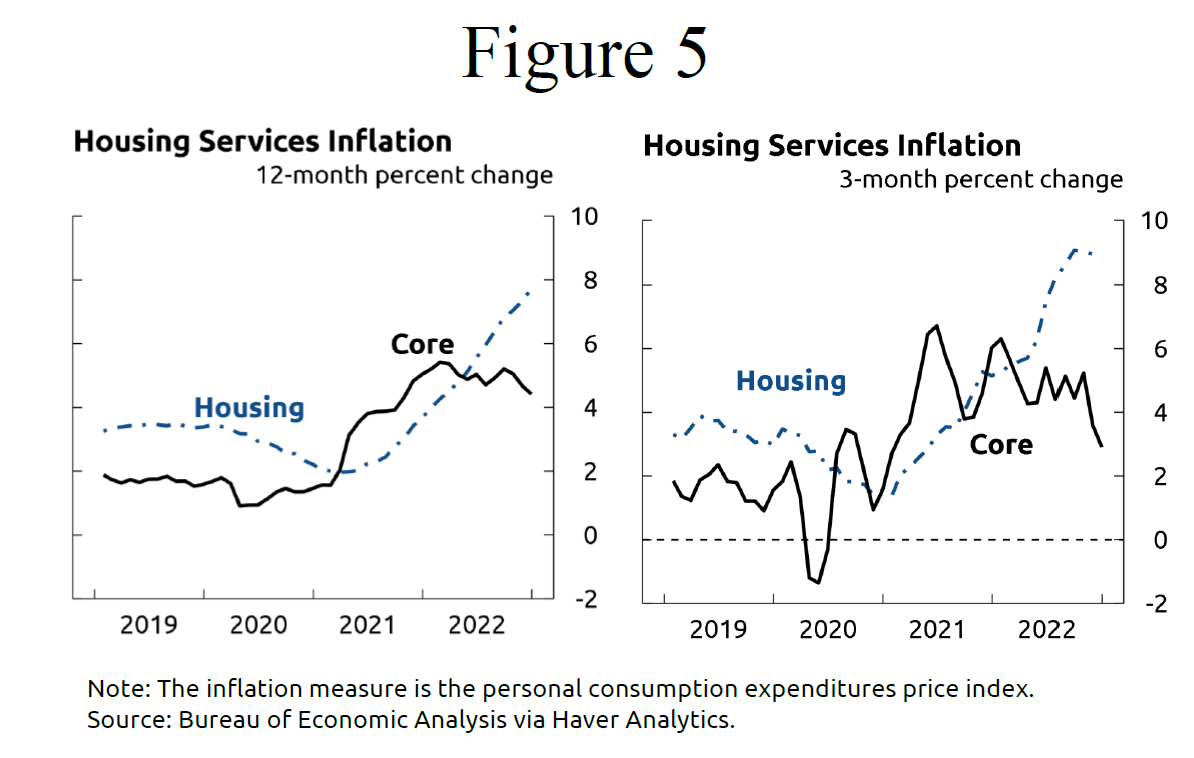

With that context, let me take a few minutes on each of the three big categories to highlight how they have been moving, and I think there is some good news. Let’s look at each category in the order of how much consumers spend on them each month. Housing services are about 15 percent of the PCE basket. Figure 5 shows how housing inflation has been evolving both when measured on a 12-month basis (left panel) and 3-month basis (right panel). As I just noted, housing inflation has been stubbornly elevated. This is true if you look at inflation over the past year or just at recent months.

{kind=link}

But high-frequency measures of market rents (for new leases by new tenants) have slowed sharply, suggesting an upcoming slowing in the rate of inflation in this part of the PCE basket. Because rents usually don’t change until leases run out, these recent declines in market rent inflation will only show through to the official inflation measure with a delay. So I expect, over time, that housing inflation will move down to be more in line with core inflation.

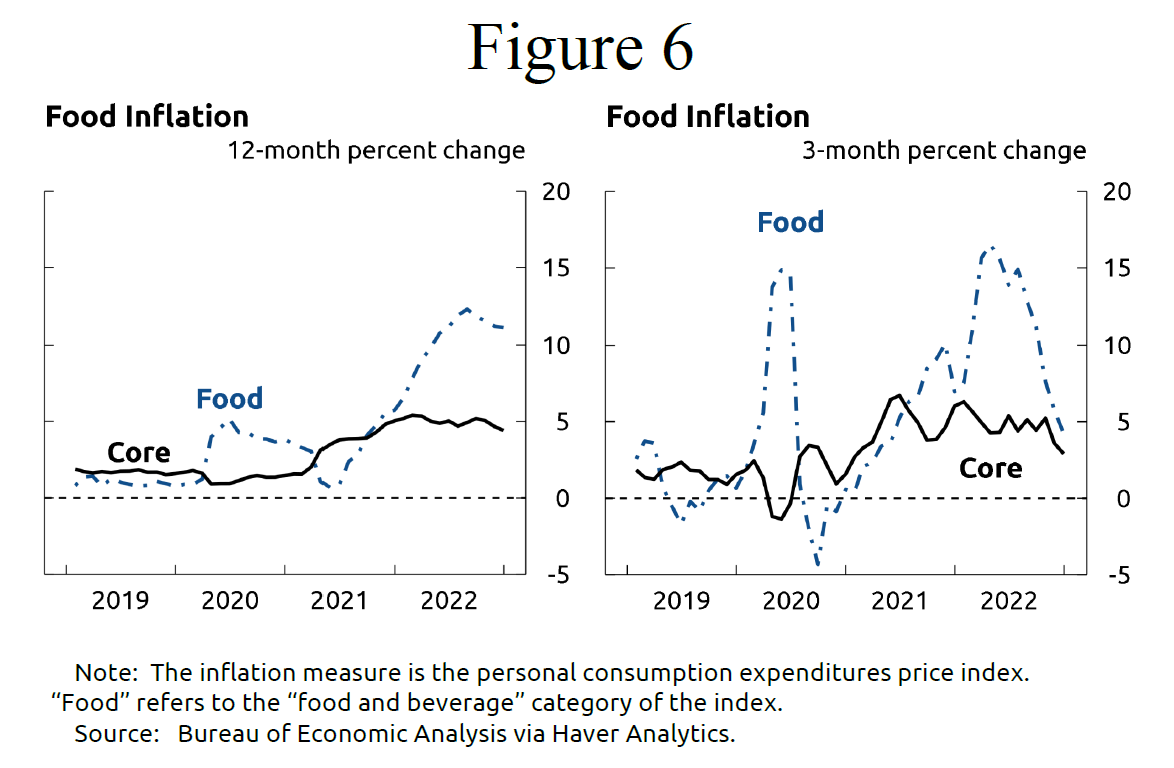

Turning to food, which represents about 7.5 percent of consumption in the PCE basket, figure 6 shows that the 12-month change in PCE food prices has greatly outpaced that of core PCE inflation over the past couple of years. More recently, we can see that the 3-month change in the PCE price index for food has slowed considerably, which is a good sign. But food inflation is still above the average annual pace of 1.1 percent over the ten years preceding the pandemic. This ongoing elevated food inflation likely reflects passthrough of the past strong increases in food commodity prices, rising labor and fuel costs, as well as supply-chain bottlenecks in packaging and transportation that have limited supplies amid strong demand.

{kind=link}

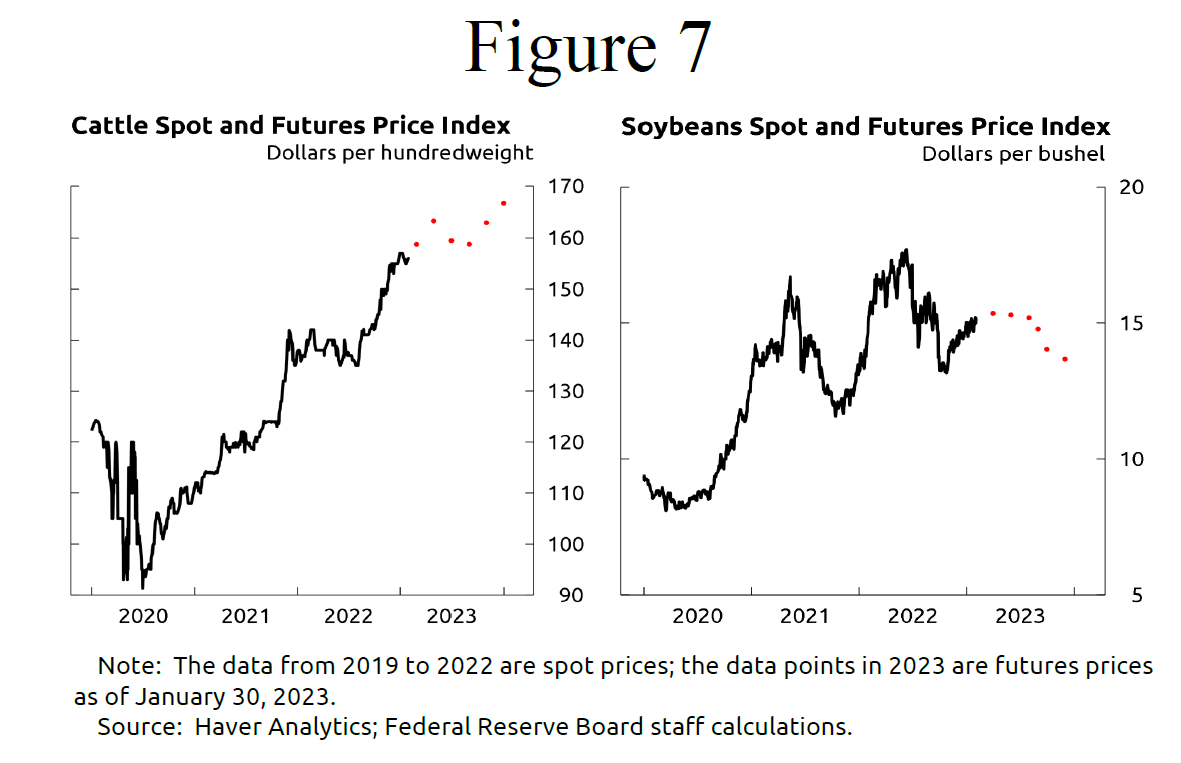

For example, as seen in figure 7, spot prices for cattle and soybeans are well above their levels at the onset of the pandemic, likely boosted by the sharply rising input costs farmers have been facing, which I discussed earlier. However, futures prices for these commodities suggest limited movements in these prices through year end. If this plays out, with a slowdown in wage increases that should occur because of tighter monetary policy, this should help continue to moderate food inflation over the next few years.

{kind=link}

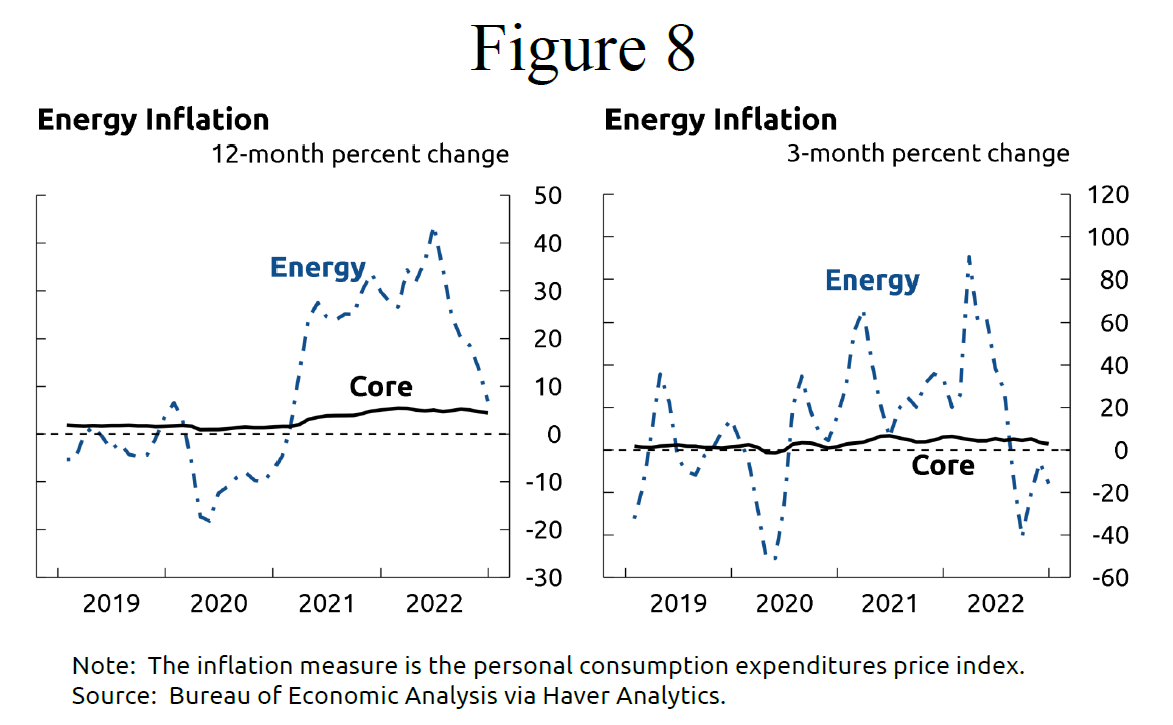

Finally, let’s turn to energy inflation. Households spend less than 5 percent of their PCE basket on gasoline, electricity, and heating but, as seen in the left panel of figure 8, the energy price index skyrocketed over the past couple of years, reflecting a surge in crude oil prices after the pandemic recession which was exacerbated by Russia’s invasion of Ukraine. Turning to the 3-month change (the right panel) energy prices have been declining sharply recently and we expect them to continue to decline this year, reflecting the path of crude oil futures prices and the expectation that unusually elevated gasoline margins will, on average, decline over the remainder of this year.

{kind=link}

So, what do I take away from all this? I think there are practical implications for getting a clear picture of the economy and setting appropriate monetary policy, and also a reminder for me about the trust I bear as a public official.

Most practically, if I had focused on core inflation over the last two years and tended to look past increases for food and energy, and especially for housing, I would have missed an alarming increase in inflation, and reacted more slowly than my Federal Reserve colleagues and I appropriately did to start bringing down inflation. The Federal Open Market Committee raised interest rates more quickly than it had in more than forty years, and I think the progress we have made on inflation shows how important it was to act so urgently.

Just as importantly, excluding those prices would have neglected how much hardship this high inflation has been for many people, especially lower-income individuals and families. High inflation is a very different experience when you are effectively paying a higher rate than others, when a higher share of your expenses and income are spent on necessities, and when you have little in savings to draw on, as lower-income people do. When I talk about how important it is to win this inflation fight, it is partly in recognition of this inescapable reality for many millions of people.

Fortunately, there are signs that food, energy, and shelter prices will moderate this year. An important factor has been the Federal Reserve’s ongoing fight to lower inflation through tighter monetary policy. We are seeing that effort begin to pay off, but we have farther to go. And, it might be a long fight, with interest rates higher for longer than some are currently expecting. But I will not hesitate to do what is needed to get my job done.