By Kristalina Georgieva, IMF Managing Director

When I took over as managing director, I thought about what the ministers and governors might ask the International Monetary Fund (IMF) next week. I conferred with David Lipton who has so ably led the Fund in this interim period. And I spoke to many of my new colleagues.

One question stood out to all of us:

What can we all do to help fix the fractures in the global economy and encourage stronger growth?

I want to begin with that this morning [October 8]. So, let’s get to it.

The Outlook

Two years ago, the global economy was in a synchronized upswing. Measured by GDP, nearly 75 percent of the world was accelerating.

Today, even more of the world economy is moving in synch but, unfortunately, this time growth is decelerating.

In 2019, we expect slower growth in nearly 90 percent of the world. [1]

The global economy is now in a synchronized slowdown.

This widespread deceleration means that growth this year will fall to its lowest rate since the beginning of the decade.

Next week we will release our World Economic Outlook which will show downward revisions for 2019 and 2020.

The headline numbers reflect a complex situation.

Despite this overall deceleration, close to 40 emerging market and developing economies are forecast to have real GDP growth rates above 5 percent — including 19 in sub-Saharan Africa.

In the United States and Germany, unemployment is at historic lows. Yet across advanced economies, including in the U.S., Japan, and especially the euro area, there is a softening of economic activity.

In some of the largest emerging market economies, such as India and Brazil, the slowdown is even more pronounced this year.

In China, growth is gradually coming down from the rapid pace it saw for many years.

The precarious outlook presents challenges for countries already facing difficulties — including some of the Fund’s program countries.

So why the slowdown in 2019? There are a range of issues and one common theme: Fractures.

I will start with trade. We have spoken in the past about the dangers of trade disputes. Now, we see that they are actually taking a toll.

Global trade growth has come to a near standstill.

In part because of the trade tensions, worldwide manufacturing activity and investment have weakened substantially. There is a serious risk that services and consumption could soon be affected.

And the fractures are spreading.

Disputes now extend between multiple countries and into other critical issues. Currencies are once again in the spotlight. Because of our interconnected economies, many more countries will soon feel the impact.

Uncertainty — driven by trade, but also by Brexit, and geopolitical tensions — is holding back economic potential.

Even if growth picks-up in 2020, the current rifts could lead to changes that last a generation — broken supply chains, siloed trade sectors, a “digital Berlin Wall” that forces countries to choose between technology systems.

Our goal should be to fix these fractures. Our world is intertwined. So our responses must be coordinated.

I believe we can do it. How? Start by unleashing the growth generating capacity of trade.

Unleash trade potential

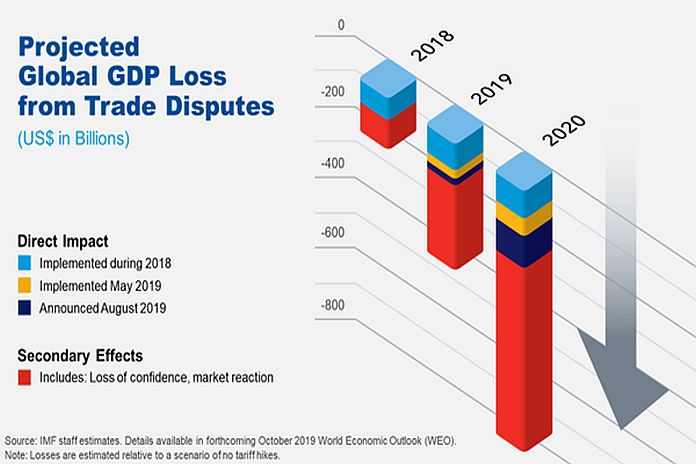

I said trade tensions were now taking a toll. Let me show you what I mean.

This graphic is part of the updated analysis on tariffs we will release next week. It shows the projected global GDP loss from the escalating trade conflict between the US and China.

The blue, yellow, and purple blocks show the direct costs on businesses and consumers from the three rounds of implemented and announced tariffs.

Now, look at the red blocks. This is what happens when the expected secondary effects are added in — including the loss of confidence and market reactions.

The results are clear. Everyone loses in a trade war. For the global economy, the cumulative effect of trade conflicts could mean a loss of around $700 billion by 2020, or about 0.8 percent of GDP. As a reference, this is approximately the size of Switzerland’s entire economy.

So we need to work together, now, and find a lasting solution on trade.

This requires difficult decisions and political will. But it is worth it.

We need real change

Countries need to address legitimate concerns related to their trade practices. That means dealing with subsidies, as well as intellectual property rights and technology transfers.

We also need a more modern global trading system, particularly to unlock the full potential of services and e-commerce.

And every country must do more to help communities harmed by the dislocations associated with technology and trade.

The key is to improve the system, not abandon it.

Access to new markets is essential to raise living standards. It is part of the answer to our question on addressing fractures. But what about the other part? Encouraging higher growth and creating more opportunity?

When it comes to improving people’s lives, the hard work starts at home. I learned this lesson first-hand growing up behind the Iron Curtain. I saw the high costs of bad policies. And I also saw how a shift to good policies, with international support, can help put a country and its people back on the path to prosperity.

So, let me focus on the domestic policy priorities we believe are critical to accelerate growth and build more resilient economies. And then I want to turn to how a renewed commitment to international cooperation — and synchronized policy action — can help us more fully address our fractures.

Policy priorities to secure stronger and more resilient growth

- Use Monetary Policy Wisely & Enhance Financial Stability

Let’s begin with monetary policy and financial stability. Central banks around the world are striving to fulfill their mandates under difficult circumstances. Their independence is the foundation of sound monetary policy.

How can they best fulfill their mandates? They should communicate their plans clearly, remain data-dependent, and where appropriate keep interest rates low. Especially since inflation is still subdued in many countries and overall growth is weakening.

However, interest rates are already very low or even negative in many advanced economies. So, in those places, there may be limited space to do more with conventional tools.

Prolonged low rates also come with negative side effects and unintended consequences. Think of pension funds and life insurance companies that are taking on more risky investments to meet their return objectives. In our surveillance, we see such an increase of risk-taking by investors broadly around the globe.

All of this creates financial vulnerabilities. In some countries, firms are using low rates and building up debt to fund mergers and acquisitions instead of investing.

Our new analysis shows that if a major downturn occurs, corporate debt at risk of default would rise to $19 trillion, or nearly 40 percent of the total debt in eight major economies. [2] This is above the levels seen during the financial crisis.

Low-interest rates are also prompting investors to search for higher yields in emerging markets. This leaves many smaller economies exposed to a sudden reversal of capital flows.

So we need macroprudential tools. And we can use new approaches to better manage debt, reduce financial booms and busts, and contain volatility.

But we should state one thing very clearly. Monetary and financial policies cannot do the job alone. Fiscal policy must play a central role.

I have heard the quip that the IMF stands for “It’s Mostly Fiscal.” Let me be true to form and focus on fiscal policy next.

- Deploy Fiscal Tools to Meet Current Challenges

Now is the time for countries with room in their budgets to deploy — or get ready to deploy — fiscal firepower. In fact, low-interest rates may give some policymakers additional money to spend.

In places such as Germany, the Netherlands, and South Korea, an increase in spending — especially in infrastructure and R&D — will help boost demand and growth potential.

That advice will not work everywhere. Globally, public debt is near record levels. So in countries with a high debt-to-GDP ratio, fiscal restraint continues to be warranted.

Countries will, of course, tailor policies that work for them. But in every country, reducing debts and deficits should always be done in a way that protects education, health, and jobs.

And every country needs to wrestle with the question of where, in a rapidly changing world, new sources of growth will come from. I believe focusing on fundamentals can help.

One way to create more fiscal space is through domestic revenue mobilization. Reducing corruption and utilizing digital tools in tax collection can unlock resources and fuel new investments in people. It can also help countries reach the 2030 Sustainable Development Goals.

- Implement Structural Reforms for Future Growth

As countries decide which policies make the most sense for this moment, we all need to keep an eye on the horizon.

Potential job losses from automation and shifting demographics require countries to reform the structure of their economies.

If we do not act, many countries will be stuck in mediocre growth.

New IMF research focused specifically on emerging markets and developing economies show how structural reforms can raise productivity and generate enormous economic gains.

These changes are the key to achieving higher growth over the medium and long-term.

The right reforms in the right sequence could double the speed at which emerging markets and developing economies reach the living standards of the advanced economies. [3]

We also know that when countries undertake reforms at the same time there can be a positive spillover effect.

Which policies work best? Let me give you some examples. [4]

- In Chile, childcare programs lifted female labor force participation and helped the economy. Proving, by the way, that empowering women is an economic gamechanger.

- In Ghana, anti-corruption legislation created more transparency and accountability.

- In Jamaica, which is completing an IMF-supported program, cutting red tape made it easier to start a new business.

These types of reforms help people find new opportunities, reduce excessive inequality, and enable countries to prepare for shocks.

Here I would like to acknowledge that today the Fund will host a conference in honor of one of our young researchers — Giang Ho — who studied many of these issues and sadly passed away last year.

To borrow a proverb from her home country of Vietnam: “ The time to jump is before your feet get wet.”

This is true. If we wait until the next crisis, it will be too late.

We need to act now. We also need to act together.

- Embrace International Cooperation

Here is what I see. While the need for international cooperation is going up, the will to engage is going down. Trade is a case in point. And yet, we need to work together. From safely adapting to fintech, to fully implementing the financial regulatory reform agenda, to fighting money laundering and the financing of terrorism.

And we need to work together to address climate change.

Climate Change

It is a crisis where no one is immune and everyone has a responsibility to act.

One of our priorities at the IMF is to assist countries as they reduce carbon emissions and become more climate-resilient.

At the current average carbon price of $2 per ton, most people and most companies have little financial incentive to make this transition. Limiting global warming to a safe level requires a significantly higher carbon price.

Some countries have embraced a straightforward strategy — taxing carbon.

Here is a good example: when Sweden introduced a carbon tax in 1991, low- and middle-income households received higher transfers and tax cuts to help offset higher energy costs. That policy shift has been instrumental in reducing Sweden’s carbon emissions by 25 percent since 1995, while its economy has grown by over 75 percent.

New research in our upcoming Fiscal Monitor confirms that carbon taxes can be one of the most powerful and efficient tools. But the key here is to change tax systems, not simply add a new tax. [5]

Additional revenues could be used to cut taxes elsewhere and fund assistance to millions of affected households. These new resources could also support investments in the clean energy infrastructure that will help the planet heal.

Dealing with climate change requires not only mitigating damage but also adapting for the future. Adaptation is about many things, but it is mostly about pricing risk and providing incentives for investment, including in new technologies.

IMF analysis from the Global Financial Stability Report shows progress is being made in the private financial sector. So-called green bonds are now on the rise in Europe and parts of Asia. [6] This is a very good development, but it is not nearly enough.

The price of inaction is high. We recognize each country faces unique challenges and constraints. But we can — and we must — cooperate on this challenge now and work together in a way that generates renewed confidence in multilateralism.

I have often said that making the case for cooperation to a more skeptical world requires delivering real results in people’s lives.

It also means reminding everyone of the power of partnership in times of crisis. This brings me to my conclusion, and a thought about our uncertain future.

Conclusion

If the global economy slows more sharply than expected, a coordinated fiscal response may be needed.

Let me be clear. We are not there. But when it comes to preparing for the possibility of a coordinated response we should remember the advice of Shakespeare:

“Better three hours too soon, than a minute too late.” [7]

Our research shows that changes in spending are more effective and have a multiplier effect when countries act together.

Or, put another way if the synchronized slowdown worsens, we may need a synchronized policy response.

We have seen how effective this approach can be in the recent past. Think about 2009 and the G20 commitment to a joint stimulus.

It is an important reminder of how countries can protect their own citizens while leveraging international cooperation for mutual benefit.

Let me conclude where I began — with the image of synchronized swimming.

The world economy is still growing, it is just growing too slowly. To reverse this trend, and meet the aspirations of people, we cannot afford to be complacent. We must act.

Next week, as our 189-member countries gather together in Washington, I urge them to come prepared to find solutions.

I am confident that if we cooperate mindful of each other’s challenges and interests we can deliver a better future for all.

{kind=link}