By Gita Gopinath

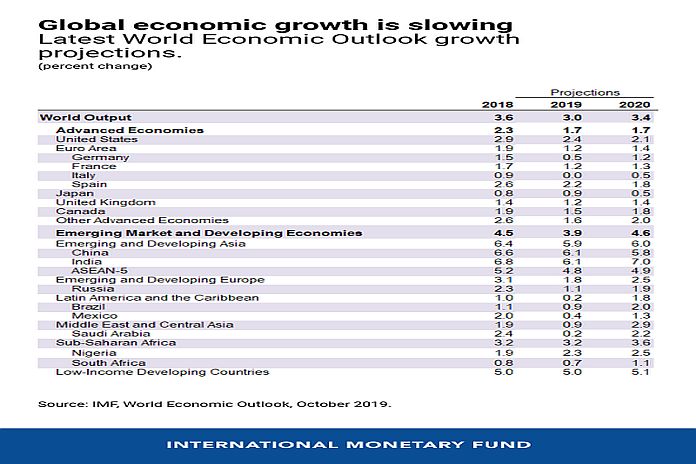

The global economy is in a synchronized slow down and we are, once again, downgrading growth for 2019 to three percent, its slowest pace since the global financial crisis. Growth continues to be weakened by rising trade barriers and increasing geopolitical tensions. We estimate that the US-China trade tensions will cumulatively reduce the level of global GDP by 0.8 percent by 2020. Growth is also being weighed down by country-specific factors in several emerging market economies, and by structural forces, such as low productivity growth and aging demographics in advanced economies.

In the October World Economic Outlook, we are projecting a modest improvement in global growth to 3.4 percent in 2020, another downward revision of 0.2 percent from our April projections. However, unlike the synchronized slowdown, this recovery is not broad-based and remains precarious.

The weakness in growth is driven by a sharp deterioration in manufacturing activity and global trade, with higher tariffs and prolonged trade policy uncertainty damaging investment and demand for capital goods. In addition, the automobile industry is contracting owing also to a variety of factors, such as disruptions from new emission standards in the euro area and China that have had durable effects. Overall, trade volume growth in the first half of 2019 has fallen to one percent, the weakest level since 2012.

We are downgrading growth for 2019 to three percent, its slowest pace since the global financial crisis.

In contrast to extremely weak manufacturing and trade, the services sector continues to hold up almost across the globe. This has kept labor markets buoyant and wage growth and consumption spending healthy in advanced economies. There are, however, some initial signs of softening in the services sector in the United States and the euro area.

Monetary policy has played a significant role in supporting growth. In the absence of inflationary pressures and facing weakening activity, major central banks have appropriately eased to reduce downside risks to growth and to prevent de-anchoring of inflation expectations. In our assessment, in the absence of such monetary stimulus, global growth would be lower by 0.5 percentage points in both 2019 and 2020.

Advanced economies continue to slow towards their lower long-term potential. Growth has been downgraded to 1.7 percent for 2019 (compared to 2.3 percent in 2018) and it is projected to stay at this level in 2020. Strong labor market conditions and policy stimulus are helping to offset the negative impact from weaker external demand for these economies.

Growth in emerging market and developing economies has also been revised down to 3.9 percent for 2019 (compared to 4.5 percent in 2018) owing in part to trade and domestic policy uncertainties, and to a structural slowdown in China.

The uptick in global growth for 2020 is driven by emerging markets and developing economies that are projected to experience a growth rebound to 4.6 percent. About half of this rebound is driven by recoveries or shallower recessions in stressed emerging markets, such as Argentina, Iran, and Turkey, and the rest by recoveries in countries where growth slowed significantly in 2019 relative to 2018, such as Brazil, India, Mexico, Russia, and Saudi Arabia. There is, however, considerable uncertainty surrounding these recoveries, especially when major economies like the United States, Japan, and China are expected to slow further into 2020.

Escalating risks

In addition, there are several downside risks to growth. Heightened trade and geopolitical tensions, including Brexit-related risks, could further disrupt economic activity and derail an already fragile recovery in emerging market economies and the euro area. This could lead to an abrupt shift in risk sentiment, financial disruptions, and a reversal in capital flows to emerging market economies. In advanced economies, low inflation could become entrenched and constrain monetary policy space further into the future, limiting its effectiveness.

Policies to reignite growth

To rejuvenate growth, policymakers must undo the trade barriers put in place with durable agreements, rein in geopolitical tensions, and reduce domestic policy uncertainty. Such actions can help boost confidence and reinvigorate investment, manufacturing, and trade. In this regard, we look forward to more details on the recent tentative deal reached between China and the United States. We welcome any steps to de-escalate tensions and to roll back recent trade measures, particularly if they can provide a path towards a comprehensive and lasting deal.

To fend off other risks to growth and to raise potential output, economic policy should support activity in a more balanced manner. Monetary policy cannot be the only game in town. It should be coupled with fiscal support where fiscal space is available, and policy is not already too expansionary. Countries like Germany and the Netherlands should take advantage of low borrowing rates to invest in social and infrastructure capital, even from a pure cost-benefit perspective. If growth were to deteriorate more severely, an internationally coordinated fiscal response, tailored to country circumstances, may be required.

While monetary easing has supported growth, it is essential that effective macroprudential regulation be deployed today to prevent mispricing of risk and excessive buildup of financial vulnerabilities.

For sustainable growth, it is important that countries undertake structural reforms to boost productivity, improve resilience, and lower inequality. Reforms in emerging market and developing economies are also more effective when good governance is already in place.

The global outlook remains precarious with a synchronized slowdown and uncertain recovery. At three percent growth, there is no room for policy mistakes and an urgent need for policymakers to support growth. The global trading system needs to be improved, not abandoned. Countries need to work together because multilateralism remains the only solution to tackling major issues, such as risks from climate change, cybersecurity risks, tax avoidance and tax evasion, and the opportunities and challenges of emerging financial technologies.

{kind=link}