The COVID-19 pandemic pushed economies into a Great Lockdown, which helped contain the virus and save lives, but also triggered the worst recession since the Great Depression. Over 75 percent of countries are now reopening at the same time as the pandemic is intensifying in many emerging market and developing economies. Several countries have started to recover. However, in the absence of a medical solution, the strength of the recovery is highly uncertain and the impact on sectors and countries uneven.

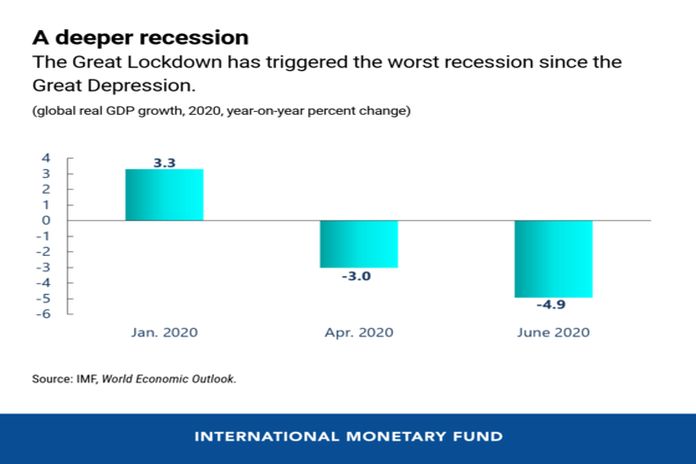

Compared to our April World Economic Outlook forecast, we are now projecting a deeper recession in 2020 and a slower recovery in 2021. Global output is projected to decline by -4.9 percent in 2020, 1.9 percentage points below our April forecast, followed by a partial recovery, with growth at 5.4 percent in 2021.

These projections imply a cumulative loss to the global economy over two years (2020–21) of over $12 trillion from this crisis.

The downgrade from April reflects worse than anticipated outcomes in the first half of this year, an expectation of more persistent social distancing into the second half of this year, and damage to supply potential.

High uncertainty

A high degree of uncertainty surrounds this forecast, with both upside and downside risks to the outlook. On the upside, better news on vaccines and treatments, and additional policy support can lead to a quicker resumption of economic activity. On the downside, further waves of infections can reverse increased mobility and spending, and rapidly tighten financial conditions, triggering debt distress. Geopolitical and trade tensions could damage fragile global relationships at a time when trade is projected to collapse by around 12 percent.

A recovery like no other

This crisis like no other will have a recovery like no other.

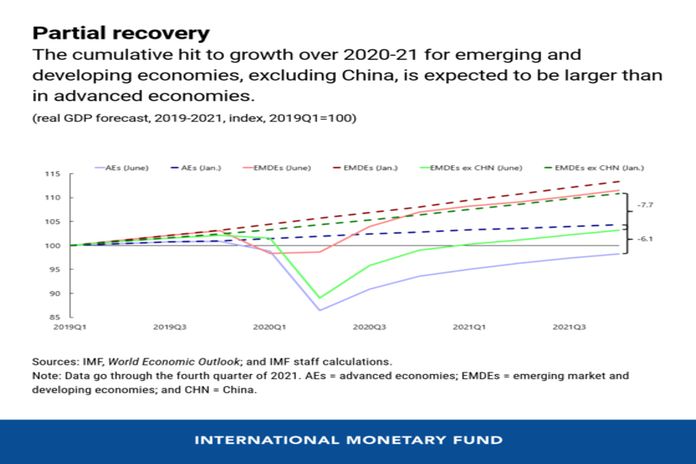

First, the unprecedented global sweep of this crisis hampers recovery prospects for export-dependent economies and jeopardizes the prospects for income convergence between developing and advanced economies. We are projecting a synchronized deep downturn in 2020 for both advanced economies (-8 percent) and emerging market and developing economies (-3 percent; -5 percent if excluding China), and over 95 percent of countries are projected to have negative per capita income growth in 2020. The cumulative hit to GDP growth over 2020–21 for emerging market and developing economies, excluding China, is expected to exceed that in advanced economies.

Second, as countries reopen, the pick-up in activity is uneven. On the one hand, pent-up demand is leading to a surge in spending in some sectors like retail, while, on the other hand, contact-intensive services sectors like hospitality, travel, and tourism remain depressed. Countries heavily reliant on such sectors will likely be deeply impacted for a prolonged period.

Third, the labor market has been severely hit and at record speed, and particularly so for lower-income and semi-skilled workers who do not have the option of teleworking. With activity in labor-intensive sectors like tourism and hospitality expected to remain subdued, a full recovery in the labor market may take a while, worsening income inequality and increasing poverty.

Exceptional policy support has helped

On the positive side, the recovery is benefitting from exceptional policy support, particularly in advanced economies, and to a lesser extent in emerging market and developing economies that are more constrained by fiscal space. Global fiscal support now stands at over $10 trillion and monetary policy has eased dramatically through interest rate cuts, liquidity injections, and asset purchases. In many countries, these measures have succeeded in supporting livelihoods and prevented large-scale bankruptcies, thus helping to reduce lasting scars and aiding a recovery.

This exceptional support, particularly by major central banks, has also driven a strong recovery in financial conditions despite grim real outcomes. Equity prices have rebounded, credit spreads have narrowed, portfolio flows to emerging market and developing economies have stabilized, and currencies that sharply depreciated have strengthened. By preventing a financial crisis, policy support has helped avert worse real outcomes. At the same time, the disconnect between real and financial markets raises concerns of excessive risk-taking and is a significant vulnerability.

We are not out of the woods

Given the tremendous uncertainty, policymakers should remain vigilant and policies will need to adapt as the situation evolves. Substantial joint support from fiscal and monetary policy must continue for now, especially in countries where inflation is projected to remain subdued. At the same time, countries should ensure proper fiscal accounting and transparency, and that monetary policy independence is not compromised.

A priority is to manage health risks even as countries reopen. This requires continuing to build health capacity, widespread testing, tracing, isolation, and practicing safe distancing (and wearing masks). These measures help contain the spread of the virus, reassure the public that new outbreaks can be dealt with in an orderly fashion, and minimize economic disruptions. The international community must further expand financial assistance and expertise to countries with limited health care capacity. More needs to be done to ensure adequate and affordable production and distribution of vaccines and treatments when they become available.

In countries where activities are being severely constrained by the health crisis, people directly impacted should receive income support through unemployment insurance, wage subsidies, and cash transfers, and impacted firms should be supported via tax deferrals, loans, credit guarantees, and grants. To more effectively reach the unemployed in countries with large informal sectors, digital payments will need to be scaled up and complemented with in-kind support for food, medicine, and other household staples channeled through local governments and community organizations.

In countries that have begun reopening and the recovery is underway, policy support will need to gradually shift toward encouraging people to return to work, and to facilitating a reallocation of workers to sectors with growing demand and away from shrinking sectors. This could take the form of spending on worker training and hiring subsidies targeted at workers that face greater risk of long-term unemployment. Supporting a recovery will also involve actions to repair balance sheets and address debt overhangs. This will require strong insolvency frameworks and mechanisms for restructuring and disposing of distressed debt.

Policy support should also gradually shift from being targeted to being more broad-based. Where fiscal space permits, countries should undertake green public investment to accelerate the recovery and support longer-term climate goals. To protect the most vulnerable, expanded social safety net spending will be needed for some time.

The international community must ensure that developing economies can finance critical spending through provision of concessional financing, debt relief and grants; and that emerging market and developing economies have access to international liquidity, via ensuring financial market stability, central bank swap lines, and deployment of a global financial safety net.

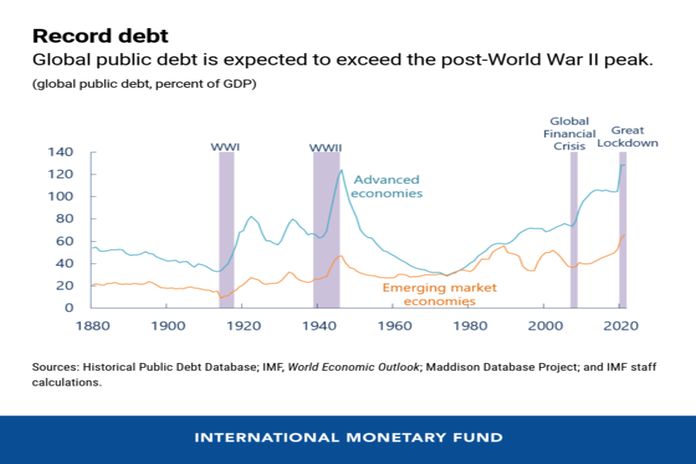

This crisis will also generate medium-term challenges. Public debt is projected to reach this year the highest level in recorded history in relation to GDP, in both advanced and emerging market and developing economies. Countries will need sound fiscal frameworks for medium-term consolidation, through cutting back on wasteful spending, widening the tax base, minimizing tax avoidance, and greater progressivity in taxation in some countries.

At the same time, this crisis also presents an opportunity to accelerate the shift to a more productive, sustainable, and equitable growth through investment in new green and digital technologies and wider social safety nets.

Global cooperation is ever so important to deal with a truly global crisis. All efforts should be made to resolve trade and technology tensions, while improving the multilateral rules-based trading system. The IMF will continue to do all it can to ensure adequate international liquidity, provide emergency financing, support the G20 debt service suspension initiative, and provide advice and support to countries during this unprecedented crisis.

![]()

{kind=link}