By Giovanni Dell’Ariccia, Paolo Mauro, Antonio Spilimbergo, and Jeromin Zettelmeyer

The COVID-19 pandemic is a crisis like no other. It feels like a war, and in many ways it is. People are dying. Medical professionals are on the front lines. Those in essential services, food distribution, delivery, and public utilities work overtime to support the effort. And then there are the hidden soldiers: those who fight the epidemic confined in their homes, unable to fully contribute to production.

In a war, massive spending on armaments stimulates economic activity and special provisions ensure essential services. In this crisis, things are more complicated, but a common feature is an increased role for the public sector.

At the risk of oversimplifying, policy needs to distinguish two phases:

Phase 1: the war. The epidemic is in full swing. To save people’s lives, mitigation measures are severely curtailing economic activity. This may be expected to last at least one or two quarters.

Phase 2: the post-war recovery. The epidemic will be under control with vaccines/drugs, partial herd immunity, and continued but less disruptive containment measures. As restrictions are lifted, the economy returns—perhaps haltingly—to normal functioning.

The success of the pace of recovery will depend crucially on policies undertaken during the crisis. If policies ensure that workers do not lose their jobs, renters and homeowners are not evicted, companies avoid bankruptcy, and business and trade networks are preserved, the recovery will occur sooner and more smoothly.

This is a major challenge for advanced economies whose governments can easily finance an extraordinary increase in expenditures even as their revenues are dropping. The challenge is even greater for low-income and emerging economies that face capital flight; they will require grants and financing from the global community (a focus for a subsequent blog).

Wartime policy measures

Unlike other economic downturns, the fall of output in this crisis is not driven by demand: it is an unavoidable consequence of measures to limit the spread of the disease. The role of economic policy is hence not to stimulate aggregate demand, at least not right away. Rather, policy has three objectives:

- Guarantee the functioning of essential sectors. Resources for COVID-19 testing and treatment must be boosted. Regular health care, food production and distribution, essential infrastructure, and utilities must be maintained. It may even involve intrusive actions by the government to provide key supplies through recourse to wartime powers with prioritization of public contracts for critical inputs and final goods, conversion of industries, or selective nationalizations. France’s early seizing of medical masks and the activation of the Defense Production Act in the United States to ensure the production of medical equipment illustrate this. Rationing, price controls, and rules against hoarding may also be warranted in situations of extreme shortages.

- Provide enough resources for people hit by the crisis. Households who lose their income directly or indirectly because of containment measures will need government support. Support should help people stay at home while keeping their jobs (government-funded sick leave reduces movement of people, hence the risk of contagion). Unemployment benefits should be expanded and extended. Cash transfers are needed to reach the self-employed and those without jobs.

- Prevent excessive economic disruption. Policies need to safeguard the web of relations among workers and employers, producers and consumers, lenders and borrowers, so that business can resume in earnest when the medical emergency abates. Company closures would cause loss of organizational know-how and termination of productive long-term projects. Disruptions in the financial sector would also amplify economic distress. Governments need to provide exceptional support to private firms, including wage subsidies, with appropriate conditions. Large programs of loans and guarantees have already been put in place (with the risks ultimately borne by taxpayers), and the EU has facilitated direct capital injections into companies by relaxing its state-aid rules. If the crisis worsens, one could imagine the establishment or expansion of large state holding companies to take over distressed private firms, as in the United States and Europe during the Great Depression.

Greater intervention by the public sector is justified by the emergency for as long as exceptional circumstances persist but must be provided in a transparent manner and with clear sunset clauses.

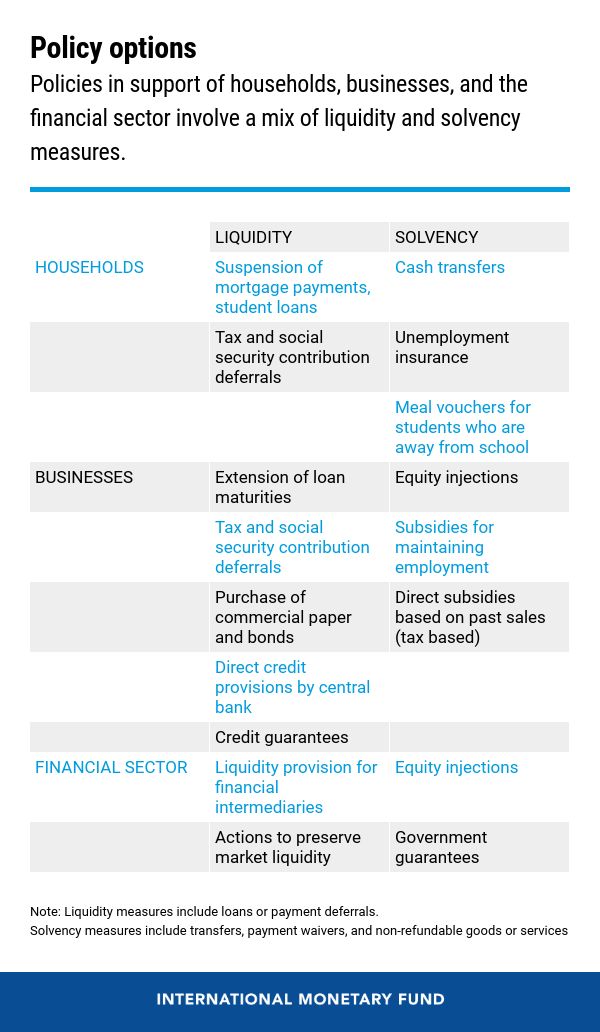

Policies in support of households, businesses, and the financial sector will involve a mix of liquidity measures (provision of credit, postponement of financial obligations) and solvency measures (transfers of real resources; see table).

Several tradeoffs will need to be managed. If transfers or subsidized loans are given to a large corporation, they should be conditional on preserving jobs and limiting CEO compensation, dividends, and stock repurchases. Bankruptcy would ensure that equity holders share some of the costs, but would also cause significant economic dislocation. An intermediate option is for the government to take an equity stake in the firm. When liquidity is the problem, credit by the central bank (through asset purchase programs) or other government-controlled financial intermediaries (through loans and guarantees) has proven effective in previous crises. Many practical questions arise also in identifying and supporting hard-hit small- and medium-sized enterprises or self-employed individuals. For these, direct transfers based on past tax payments should be considered.

These domestic policies need to be supported by maintaining international trade and cooperation, which are essential to defeating the pandemic and maximizing the chances of a quick recovery. Limiting the movement of people is necessary for containment. But countries must resist the instinct of shutting down trade, especially for health-care items and the free exchange of scientific information.

From shelter-in-place to recovery

Promoting the recovery will have its own challenges, including higher levels of public debt and possibly new swaths of the economy under government control. But relative success in Phase 1 will ensure that economic policy can go back to its normal operation. Fiscal measures to boost demand will become increasingly effective as more people are allowed to leave their homes and go back to work.

Interest rates and inflation were projected to be low-for-long prior to the pandemic in most advanced economies. Preventing major disruptions in supply chains should avoid inflation during the emergency and recovery phases. If the measures to contain the spread of the virus are successful, the necessary increase in the public debt ratio will have been sizable, but interest rates and aggregate demand are likely to remain low in the recovery phase. Under those circumstances, fiscal stimulus will be appropriate and highly effective in most advanced economies. And this will facilitate exit from the exceptional measures introduced during the crisis.

![]()

{kind=link}