By

By {kind=link}

Inflation is many things. It’s the invisible thief of purchasing power, a distorting mirror for investment, and, occasionally, a necessary grease for the wheels of the economy to run. Once a dormant beast in the developed world, since the pandemic, inflation has instead become a primary concern for central bankers, politicians and the person in the street.

Defining inflation in economics: How does it work?

At its simplest, inflation is the rate at which the general level of prices for goods and services (the cost of living) is rising, and, subsequently, purchasing power is falling. It is not merely the price of a single steak or a gallon of petrol going up; it is a broad-based increase in prices across the economy.

Inflation alters the incentives of every economic actor. When money loses value, holding cash becomes a losing proposition. This encourages spending and investment in the short term but can lead to long-term instability if the pace of price changes becomes unpredictable. Inflation acts as a tax on those with variable-rate loans or fixed incomes and a boon to those with fixed-rate debts. The complexity lies in its transmission: How does a hike in energy prices or a surge in the money supply filter through the myriad layers of a modern, globalized supply chain?

What is the Consumer Price Index (CPI) and consumer inflation?

The Consumer Price Index (CPI) serves as the most prominent yardstick for inflation. It represents a ‘basket of goods’ meant to mirror the spending habits of an average urban household. This basket includes everything from the mundane, loaves of bread and haircuts, to the significant, such as rent, fuel and healthcare.

Measuring consumer inflation is a tricky business. National statistics bureaus track the prices of thousands of items monthly. However, the CPI is not a static list. It utilizes ‘weights’ based on expenditure shares. If households spend more on technology and less on tobacco, the index is normally rebalanced to reflect this shift.

Critically, the CPI is often subject to ‘hedonic adjustments’. This is the process where statisticians account for quality improvements. If a laptop costs the same this year as last but is twice as fast, the ‘price’ has effectively fallen in the eyes of the CPI. While in theory sound, this often leads to a disconnect between official data and the ‘sticker shock’ felt by consumers at the checkout counter.

Core inflation vs. headline inflation: Key differences

For the casual observer, inflation is inflation. But for the central banker at the Federal Reserve or European Central Bank, the distinction between headline and core inflation is crucial.

Headline inflation is the raw, unadjusted figure. It includes everything in the CPI basket, most notably food and energy. These two categories are notorious for their volatility. For instance, the recent geopolitical flare-up in the Middle East has shoved up energy prices, causing headline inflation to spike around the world. These spikes are often ‘transitory’, and they may reverse as quickly as they appeared.

Core inflation, conversely, strips away these volatile food and energy costs. It is designed to capture the underlying trend of price changes—the ‘signal’ rather than the ‘noise’. Central banks focus more on core inflation because it reflects domestic economic pressures, such as wage growth and service costs, which are more driven by changes in interest rates at home. If core inflation is rising, it suggests that price increases are becoming embedded in the economy, requiring a firm hand from the monetary authorities.

Why inflation can be good: The Philips Curve and economic growth

The common instinct is to view any price increase as a bad thing. However, an economy of zero inflation (or worse, falling prices) is often a stagnant one. Most developed-economy central banks target a 2.0 percent inflation rate for a reason: It provides a ‘buffer’ against deflation and allows the labor market to function more smoothly. In an economy where wages are ‘sticky’, meaning workers fiercely resist nominal pay cuts, modest inflation allows real wages to adjust downwards during downturns without the need for mass layoffs.

The Philips Curve: Balancing unemployment and prices

One of the most enduring, albeit controversial, frameworks in macroeconomics is the Philips Curve. Historically, it suggested an inverse relationship between unemployment and inflation. The logic was straightforward: When unemployment is low, the labor market is tight. Workers have more leverage to demand higher wages. To cover these costs, firms raise prices. Thus, low unemployment leads to higher inflation.

In the modern era, this relationship has ‘flattened’. During the 2010s, many economies saw record-low unemployment with almost no inflation. However, the post-2020 era saw the curve return with a vengeance. Central banks must find the ‘NAIRU’ (Non-Accelerating Inflation Rate of Unemployment)—the sweet spot where the economy is at full capacity without causing prices to spiral. Pushing unemployment too low can overheat the engine; allowing it to rise too high causes social misery. It is a delicate balancing act that defines the tenure of every central bank governor.

Why inflation is better than deflation for the economy

If inflation is the erosion of money, deflation is its petrification. On the surface, falling prices sound delightful for the consumer. In reality, persistent deflation is an economic poison. When prices fall, consumers delay purchases, expecting goods to be even cheaper next month. Weaker consumer spending leads to a collapse in demand, which forces firms to cut production and lay off workers, potentially creating a deflationary spiral.

Moreover, deflation increases the ‘real’ burden of debt. If you owe $100,000 and prices (and wages) are falling, that debt becomes effectively larger relative to your income. This can lead to a situation where defaults rise, banks stop lending, and the economy grinds to a halt. Inflation, at a moderate and predictable level, encourages people to spend and invest today rather than hoarding cash under a mattress. It keeps the ‘velocity’ of money healthy and ensures that the future remains something worth investing in.

The Dark Side: What leads to high inflation and stagflation?

When inflation breaks its leash, the consequences can be catastrophic. High inflation erodes the social contract. It punishes the thrifty who saved for retirement and rewards those who took on excessive debt. It creates a ‘tax’ that falls most heavily on the poor, who spend a larger share of their income on essentials and have fewer assets, like property or stocks, that rise in value along with inflation.

What causes inflation? Demand-Pull vs Cost-Push

To treat inflation, one must first diagnose its source. Economists generally categorise the ‘why’ into two buckets:

- Demand-Pull Inflation:This occurs when the total demand for goods and services exceeds the economy’s capacity to produce them. It is the classic case of ‘too much money chasing too few goods’. This is often fueled by low interest rates, excessive government spending, or a sudden surge in consumer confidence. The economy overheats, and prices are pulled upward by the sheer force of demand.

- Cost-Push Inflation:This is driven by the supply side. When the costs of production (wages, raw material costs or energy) rise significantly, firms pass these costs onto consumers to maintain profit margins. The 1970s oil shocks are the textbook example. In the last few years, we have seen cost-push elements driven by war in Ukraine, tariffs, supply chain disruptions and decoupling, the green transition and, most recently, geopolitical conflict in the Middle East.

Stagflation and the risks of hyperinflation

The most dreaded portmanteau in economics is stagflation: A combination of stagnant economic growth and high unemployment and inflation. It is a policy nightmare because the tools used to fight inflation (raising interest rates) typically increase unemployment and slow growth further. Conversely, tools used to stimulate growth (lowering rates) risk fueling the inflationary fire. Stagflation usually results from a massive supply shock that breaks the traditional Philips Curve trade-off. There are concerns that US and Israeli attacks on Iran, and Iran’s subsequent blockage of the Hormuz Strait, could cause such stagflation if conflict is prolonged.

Hyperinflation, while rarer, represents a total loss of confidence in a nation’s currency. This is not merely ‘high’ inflation; it is inflation that has gone exponential, often exceeding 50 percent per month. It is almost always a political failure rather than a purely economic one. When a government can no longer tax its citizens or borrow from markets, it resorts to the printing press to fund its obligations. The result is a currency that loses value by the hour.

Disadvantages and consequences of High Inflation

Beyond the headline numbers, high inflation creates a ‘noise’ that distorts economic decision-making.

- Menu Costs: Named for the cost to a restaurant of constantly printing new menus, this refers to the administrative costs firms face when they must frequently update prices.

- Price Signal Distortion: In a healthy economy, price changes tell us what is scarce and what is abundant. High inflation masks these signals. Is the price of milk up because milk is scarce, or just because of currency devaluation? When businesses can’t tell the difference, they misallocate capital.

- Fiscal Drag: As nominal wages rise with inflation, workers are often pushed into higher tax brackets even though their ‘real’ purchasing power hasn’t increased. This is a stealth tax hike that further dampens economic dynamism.

From hyperinflation to disinflation: How price trends vary globally

The global inflation map remains a patchwork of extremes. At least until the Iran war broke out, many developed-country central banks had succeeded in reducing inflation to near their 2.0 percent targets. Meanwhile, some countries are experiencing double- and even triple-digit inflation, while others are flirting with falling prices.

High inflation dynamics: The case studies of Argentina and Venezuela

Argentina remains one of the world’s cautionary tales when it comes to inflation. Decades of fiscal profligacy and a lack of central bank independence have led to a lack of confidence in the currency and a culture of ‘inflationary expectations’. When everyone expects prices to rise by 100 percent next year, they set their prices and wage demands accordingly, making the expectation a self-fulfilling prophecy. This has led to repeated rounds of hyperinflation. The most recent such bout of price pressures peaked in early 2024 with annual Argentinian inflation at around 290 percent. Inflation has come down since, but is still among the highest in the world at over 30 percent. This is despite austere fiscal policy under president Milei, highlighting how inflation can become entrenched and difficult to eradicate.

Venezuela offers an even darker look at hyperinflation. Since 2013, the destruction of the domestic productive base, combined with sanctions and catastrophic mismanagement of the oil sector, led to a currency that became more valuable as wallpaper than as money. This caused Venezuelan inflation to peak at well over 100,000 percent towards the end of the 2010s. Price pressures have come down since, though a renewed episode of currency collapse from late 2024 onwards drove inflation back above 600 percent in early 2026. The lesson, as in the case of Argentina, is clear: Once the public loses faith in the ‘store of value’ function of a currency, the path back to stability is long and painful, requiring a total overhaul of the political and institutional framework.

Low inflation and disinflation risks: Insights on China and Switzerland

At the other end of the spectrum lie countries such as China and Switzerland. China, throughout 2025 and 2026, has flirted with disinflation (a slowing of the rate of inflation) and outright deflation. A massive property market slump and high youth unemployment have dampened domestic demand and demand-pull price pressures. Moreover, the country’s vast manufacturing capacity and vicious price wars between firms, with the EV sector a prime example, have further weighed on Chinese prices on the supply side. For China, the risk is ‘Japanification’: a multi-decade period of stagnant prices and low growth that is notoriously difficult to escape.

Switzerland is another country that has flirted with deflation recently, marking a return to the extremely low price pressures of the 2010s. This is partly due to the strength of the Swiss franc, which makes imports cheaper, and a highly productive, high-value economy that can absorb cost increases without passing them all to consumers. Further drivers of absent inflation in Switzerland are muted wage growth and strong domestic nuclear and hydroelectric energy capacity, which limits imported inflation when global energy prices surge.

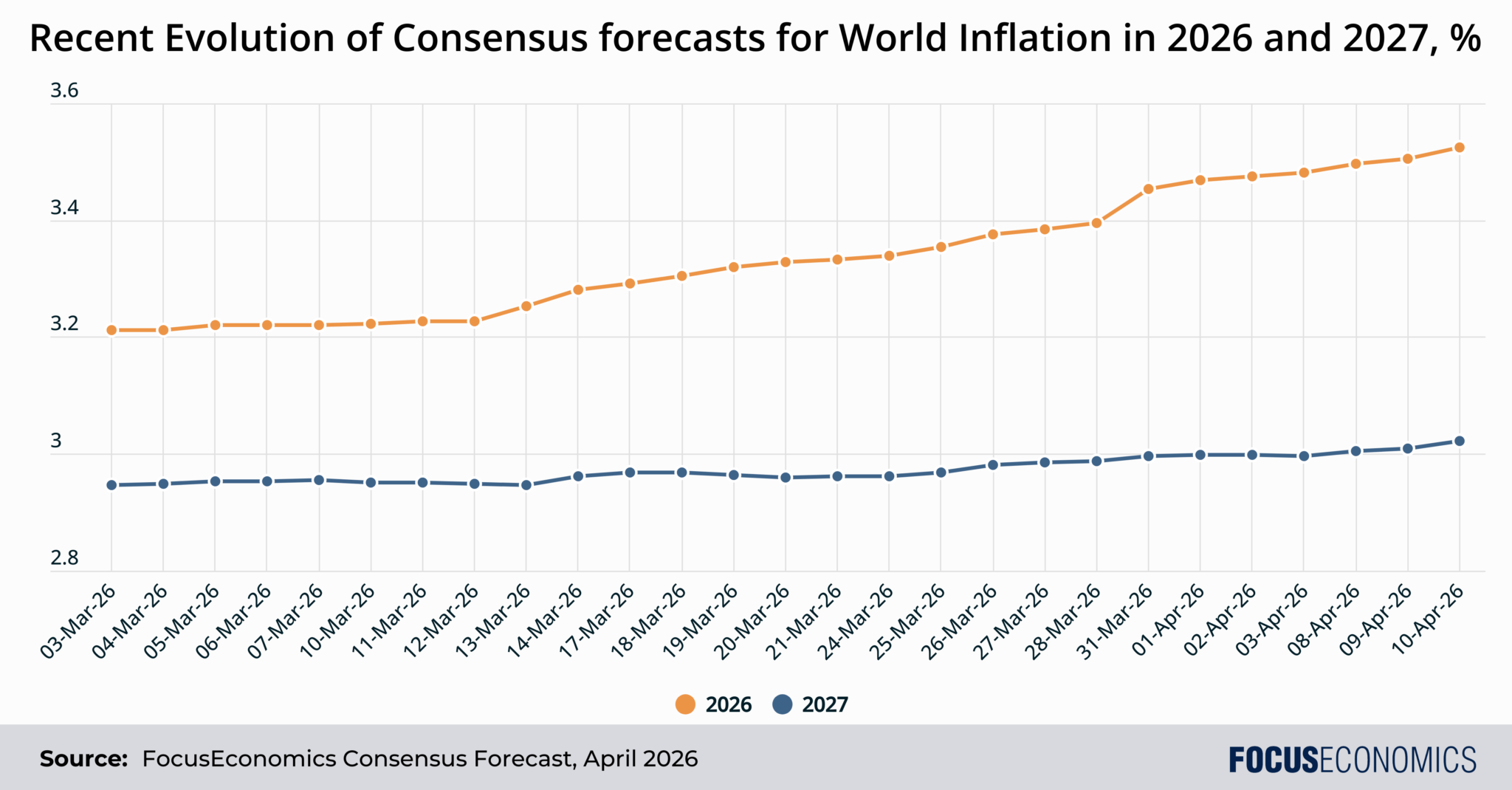

Our Inflation Consensus Forecasts

On aggregate, the hundreds of panelists that we poll expect global inflation to average 3.6 percent in 2026 and 3.1 percent in 2027. The 2026 figure has been revised up by over 0.3 percentage points since the outbreak of war in the Middle East at the end of February, as the below chart shows:

However, inflation is still seen averaging close to 2025 levels this year, and should then dip in 2027 as energy prices pull back. A prolonged Middle East war is a key upside risk.

The extreme discrepancy between countries will persist going forward. Venezuela should see the highest inflation this year at 407 percent, as a result of rapid currency weakening. At the other end of the spectrum is the West Bank and Gaza, which is forecast to see consumer prices fall 15 percent as reduced conflict-related disruption aids the supply of goods.

Summing up

A key lesson since the pandemic, and particularly now that war threatens an inflation resurgence, is that price stability is not a natural state of affairs. Rather, it is a result of institutional design, political will and a stable geopolitical backdrop. If one or more of these factors are lacking, higher inflation is the likely result.

That links to another lesson: When inflation does emerge, the cost of it getting out of hand is almost always higher than the cost of reining it in.