{kind=link}

By FocusEconomics

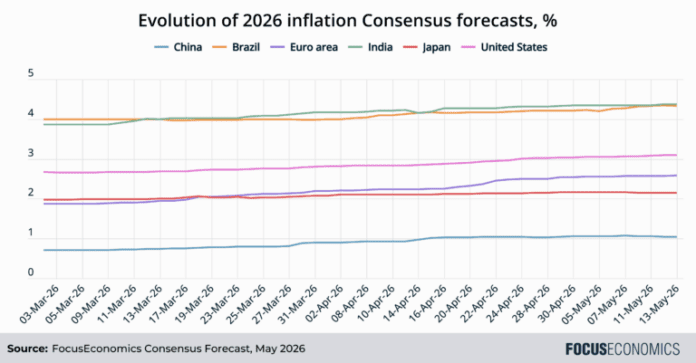

Higher energy prices act as catalyst: Since the US and Israel attacked Iran on 28 February, Brent crude oil prices and natural gas prices in Asia and Europe have both risen around 50 percent. This has led our panelists to upgrade their inflation forecasts for economies all across the world, as the chart below shows:

Policy rate forecasts rise in tandem: This has in turn caused panelists to increase their projections for the end-2026 policy rate in many countries, as central banks are likely to keep rates higher than was planned before the Iran war in order to ward off inflation. Among G7 and BRIC economies, end-2026 policy interest rate forecasts have risen the most in Brazil.

This time is different: However, global interest rates are likely to remain below the peak reached in early 2024, and are still seen declining gradually later this year vs current levels. Though the recent energy price jump is similar in scope to that observed after Russia invaded Ukraine in 2022, there isn’t the same pent-up post-pandemic consumer demand that led to an inflation surge in 2022–2023 and sharp monetary tightening across the world. Moreover, governments are now being more proactive with measures to offset higher prices at the pump, with many already implementing VAT and excise duty waivers for instance.

Risks are to the upside: Our panelists’ policy rate forecasts are likely to rise further going forward unless the Hormuz Strait reopens. This is because energy prices could lurch higher as global stockpiles dry up and new fuel fails to move from the Gulf to the rest of the world in sufficient quantities, necessitating tighter monetary policy. Even if conflict in the Middle East resolves and the Hormuz Strait fully opens, energy prices are likely to stay above pre-March levels for several quarters. Energy output will take time to ramp up, especially given damage to Gulf energy facilities from Iranian drone strikes. Moreover, shipping insurance costs could remain above pre-war levels due to fear of conflict resuming, introducing an effective surcharge to energy prices that wasn’t there before. All this will buoy up inflation and interest rates in turn.

On the Fed’s stance, EIU analysts said:

“We expect the Fed to keep the target range for the policy rate unchanged in the first half of the year as it gauges the impact of the 2025 easing and assesses a vastly more complicated inflation outlook. Although softer activity and labour-market data would ordinarily support renewed easing later in the year, the Iran war has raised oil prices and broader energy prices sharply, boosted headline inflation and increased the risk that higher energy costs feed into core inflation and inflation expectations. We therefore now expect just one additional 25-basis-point cut, in the fourth quarter of 2026, taking the policy rate to a range of 3.25-3.5 percent, followed by one further cut in the first quarter of 2027.”

On the euro area policy rate, ING’s Carsten Brzeski said:

“Back in 2011, the ECB hiked interest rates – admittedly from slightly lower levels than currently – to tackle rising inflationary pressures. Only to find out that these rate hikes pushed the eurozone economy further into stagnation. As the ECB had underestimated the adverse effects of the sovereign debt crisis, the 2011 rate hikes were reversed quickly. Underestimating the adverse impact of a shock and focusing too much on rising inflation as a result of higher energy prices? The ECB has been there. […] It’s still hard to see that the ECB would really want to fight an exogenous supply shock at the cost of worsening an economic downturn. However, a rate hike, be it symbolic or even a policy mistake, at the June meeting has clearly become more likely.”

On China, United Overseas Bank’s Ho Woei Chen said:

“Higher inflation itself is not necessarily bad for China’s economy after more than three years of deflationary pressure. However, inflationary pressures that were driven by supply-side factors against subdued demand is a less desirable phenomenon. A more constructive outcome would be a reversal of entrenched low-price expectations, leading to demand-driven price pressures supported by resilient domestic growth. The PBOC remains on course to keep its monetary policy “moderately loose” to support the consumption recovery. However, we no longer expect the PBOC to cut interest rates this year vs. our previous forecast of a modest 10 bps cut in 3Q26. We also see less prospects of a 25-50 bps cut in the reserve requirement ratio (RRR) in 2026.”